Author: Senior Insurance Consultant (20+ Years Experience)

In my two decades of advising clients—from young families just starting out to high-net-worth individuals planning their estates—the single most common question I receive is: “Should I buy Term or Whole Life insurance?”

It is not just a question of preference; it is a question of financial trajectory. According to LIMRA’s 2024 Insurance Barometer Study, a record-high 42% of Americans—representing 102 million adults—say they need more life insurance. Yet, many remain paralyzed by analysis paralysis, fearing they will choose the “wrong” product.

Here is the brutal truth the brochures often gloss over: For 90% of the population, the answer is simple. For the other 10%, the nuance is critical. This guide cuts through the sales jargon to give you a factual, data-grounded comparison to help you protect your financial legacy.

At a Glance: The Core Differences

Before we dive deep, let’s look at the numbers. The following table compares a standard policy for a healthy 30-year-old male seeking $500,000 in coverage, based on 2024/2025 market averages.

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Duration | Temporary (10, 20, 30 years) | Permanent (Until death/age 100+) |

| Monthly Cost (Approx.)* | ~$26 | ~$440 – $451 |

| Cash Value | None (Pure protection) | Accumulates over time (Tax-deferred) |

| Primary Purpose | Income replacement during working years | Estate planning, legacy, forced savings |

| Lapse Risk | Low (Simple to maintain) | High in early years (Due to high cost) |

*Data Source: 2024/2025 average premium data from Policygenius and NerdWallet for a healthy 30-year-old male, $500k coverage.

Understanding Term Life Insurance: The “Rent” Option

Think of Term Life Insurance as renting coverage. You pay a monthly premium to “rent” a death benefit for a specific period—usually 10, 20, or 30 years. If you pass away during that time, your beneficiaries get the money tax-free. If you outlive the term, the policy expires, and you walk away with nothing.

While “walking away with nothing” sounds like a loss, it is actually the feature that makes Term insurance so affordable. Because the insurance company knows the vast majority of term policies will expire without a claim, they can offer massive coverage for the price of a takeout dinner.

The 2024 Market Shift

In 2024, we are seeing a resurgence in Term Life. With inflation squeezing household budgets, families are prioritizing pure protection over investment-heavy products. LIMRA reports that Term Life premiums are on pace to reach $3 billion in 2024, a new sales record. This indicates that consumers are becoming smarter about separating their insurance from their investments.

Pros of Term Life

- Affordability: It is roughly 15-20x cheaper than Whole Life for the same death benefit.

- Simplicity: No hidden fees, surrender charges, or complex dividend rates to track.

- Flexibility: You can match the term to your financial obligations (e.g., a 20-year term to cover a 20-year mortgage).

Cons of Term Life

- Expiration: Once the term ends, renewing is often prohibitively expensive.

- No Equity: You do not build up any cash value or savings within the policy.

Understanding Whole Life Insurance: The “Buy” Option

Whole Life Insurance is like buying a home. You pay significantly higher premiums, but a portion of that money goes into a “cash value” account that grows over time. The policy is permanent; as long as you pay the premiums, it will pay out when you die, whether that is tomorrow or at age 99.

The “Cash Value” Component

This is the most misunderstood aspect of insurance. In a Whole Life policy, your premiums are split. One part pays for the cost of insurance (mortality risk), administrative fees, and sales commissions. The remainder goes into a cash value account, which grows at a guaranteed rate set by the insurer.

However, caveat emptor (buyer beware): In the first few years, almost 100% of your premium goes toward fees and commissions. It often takes 10 to 15 years for the cash value to equal the total premiums you have paid. This “break-even” point is a crucial reality check for anyone viewing this strictly as an investment.

Pros of Whole Life

- Permanence: Guaranteed payout (death benefit) as long as premiums are paid.

- Forced Savings: Builds an asset you can borrow against in emergencies.

- Tax Advantages: Cash value grows tax-deferred, and loans against the policy are generally tax-free.

Cons of Whole Life

- Cost: The high premiums ($450+ vs. $26) make it difficult for average families to afford sufficient coverage.

- Complexity: Understanding dividend scales, surrender charges, and loan interest rates requires financial literacy.

- Lapse Rates: Because of the high cost, many people stop paying. Industry data suggests nearly 15% of whole life policies lapse within the first five years, often resulting in a total loss of premiums paid.

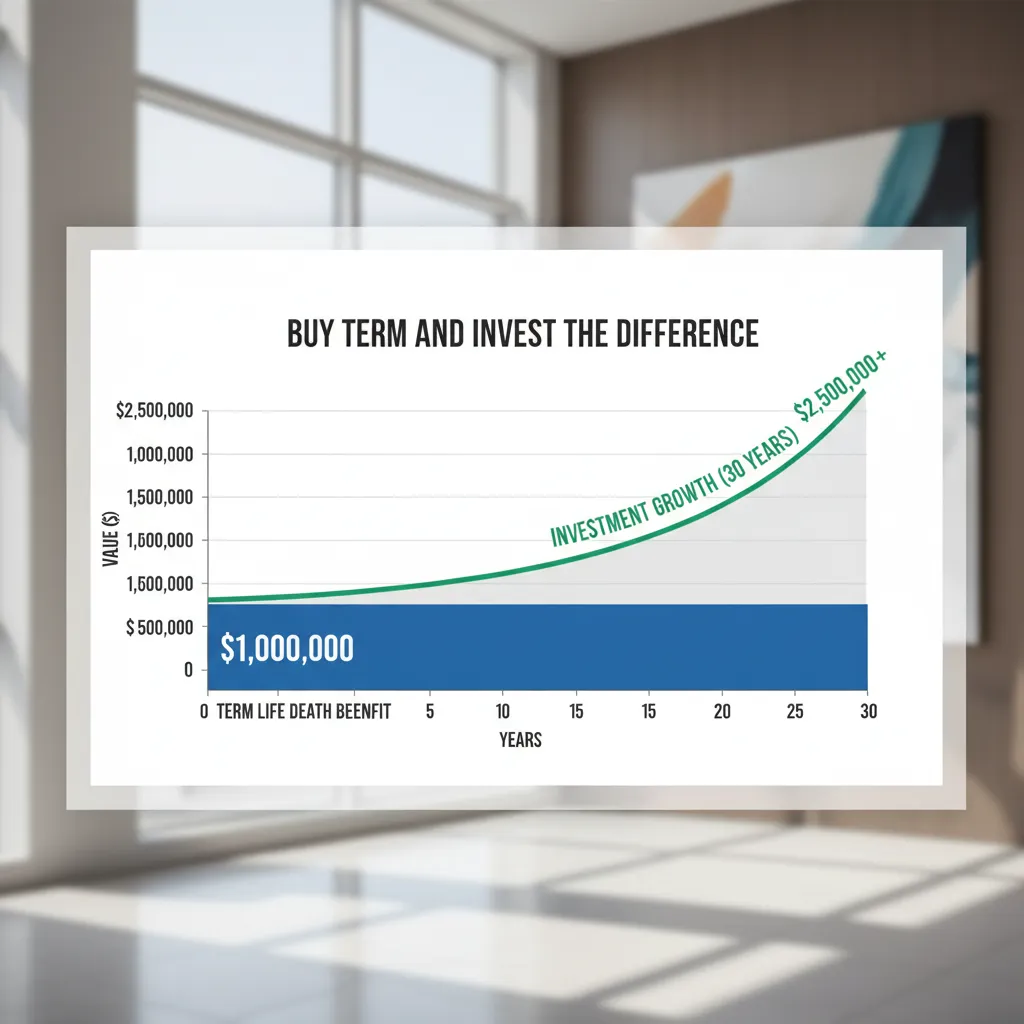

The “Buy Term and Invest the Difference” Strategy

This is the classic financial advice argument, and the math is compelling. Let’s look at a real-world scenario using the 2024 cost data we cited earlier.

The Scenario: You are 30 years old and have $450 per month budgeted for financial security.

- Option A (Whole Life): You buy a $500,000 Whole Life policy. You pay $450/month. If you die, your family gets $500,000. You have some cash value growing slowly.

- Option B (Term + Invest): You buy a $500,000 Term policy for $26/month. You take the remaining $424 and invest it in a diversified index fund averaging a 7% annual return.

The Result after 30 Years:

- Option A: You likely have a cash value of around $200,000 – $250,000 (depending on dividends). Your death benefit remains $500,000 (unless you purchased paid-up additions).

- Option B: Your investment account would have grown to approximately $500,000. You effectively “self-insured.” If you die, your family gets the investment account plus the term insurance (if still active) or just the investments (if the term expired).

For disciplined investors, Option B usually yields higher wealth. However, it requires the discipline to actually invest that difference every single month.

Decision Framework: Which One is Right for You?

As a consultant, I don’t believe in “one size fits all.” Here is how I categorize clients based on their specific needs.

Choose Term Insurance If:

- You have high financial obligations but limited cash flow. (e.g., Young parents, new homeowners).

- You need maximum coverage. If you need $1 million to protect your family, Term might cost $50/month, while Whole Life could cost $1,000+. It is better to have the full $1 million in Term than a $50,000 Whole Life policy that leaves your family underinsured.

- You want simplicity. You want protection, not another complex financial asset to manage.

Choose Whole Life Insurance If:

- You have a lifelong dependent. If you have a child with special needs who will require care after you are gone, permanent insurance ensures funding is there regardless of when you pass.

- You have maxed out all other tax-advantaged accounts. If you have already maxed your 401(k) and IRA and are looking for a conservative, tax-sheltered place for excess cash.

- Estate Tax Planning. For ultra-high-net-worth individuals (estates over $13.61 million in 2024), Whole Life can provide liquidity to pay estate taxes without liquidating other assets.

Conclusion: The Verdict

Insurance is meant to be a safety net, not a lottery ticket. For the vast majority of Americans—especially those in the wealth-accumulation phase of life—Term Life Insurance is the superior choice. It provides the high coverage your family needs at a price that allows you to invest in your future simultaneously.

Whole Life Insurance is a specialized tool. It is not a “scam,” but it is often oversold to people who would be better served by Term. Before committing to a Whole Life policy, ask yourself: “Am I buying this for protection, or am I trying to combine investing with insurance?” Usually, keeping them separate is the winning strategy.

Frequently Asked Questions (FAQ)

Do I get my money back at the end of a Term Life policy?

Generally, no. Standard term insurance is “pure protection,” similar to car insurance. If you don’t crash your car, you don’t get your premiums back. However, there is a rider called “Return of Premium” (ROP), which refunds your payments if you outlive the term, but this typically doubles or triples the monthly cost.

Can I convert my Term policy to Whole Life later?

Yes, most reputable term policies include a “conversion rider.” This allows you to convert some or all of your term coverage into a permanent policy without undergoing a new medical exam. This is a valuable feature if your health deteriorates during the term.

Is Whole Life insurance a good investment in 2024?

Compared to the stock market (S&P 500), Whole Life historically offers lower returns (typically 3-5% internal rate of return over the long haul). However, it is considered a “safe” asset class that is not correlated with stock market volatility. It should be viewed as a conservative bond alternative, not a high-growth investment.

Why are Whole Life premiums so much higher?

Whole Life premiums are higher because the payout is guaranteed (everyone dies eventually), whereas Term policies rarely pay out (most people outlive the term). Additionally, the premiums must fund the cash value account and cover higher administrative costs and commissions.